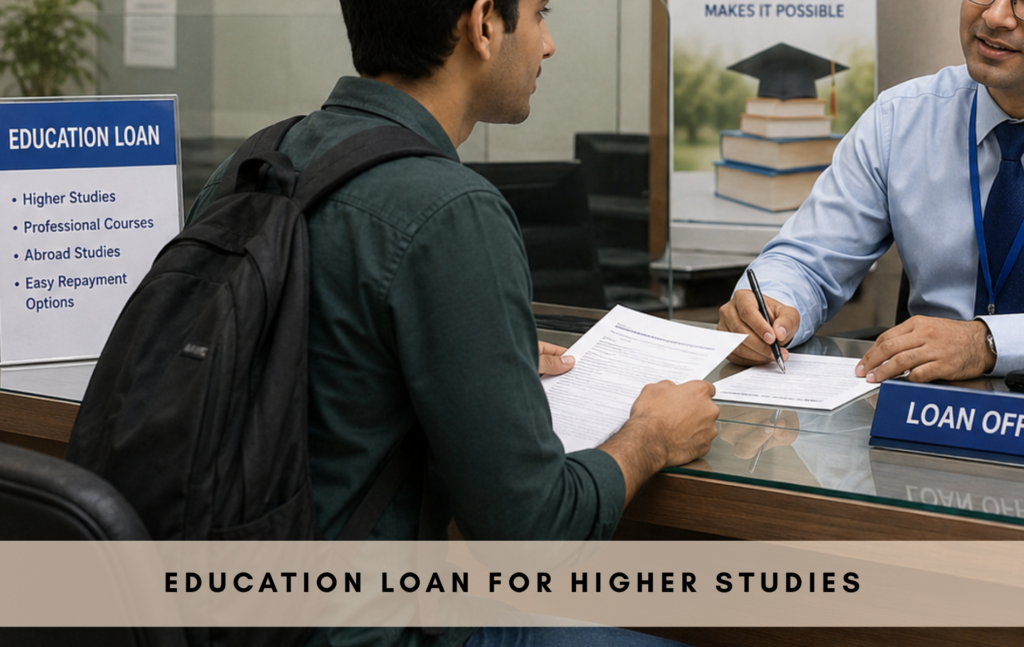

Education Loan in India: In the present day’s competitive world, it is a wish of lots of students to get higher education in India or abroad. But as tuition and living costs continue to soar, many middle-class families are finding it increasingly difficult to pay for that dream. Now, this is exactly where an education loan in india comes in as a financial savior.

If you’re, or planning to be, a professional course taker such as, MBA, B.Tech, MBBS or PhD then this all comprehensive guide will take you through the entire process securing a loan from any bank seamlessly.

1. Types of Education Loans Available

You will need to know what kind of financial help you will require before you can go to the bank. Education loans in India can be broadly classified as:

- Secured Loans (With Collateral): You need to pledge an asset such as residential property, land, Fixed Deposits, or LIC policies as security against the loan. The good thing is that you can obtain bigger loan with lower interest rate.

- Unsecured Loans (Without Collateral): You need no collateral to obtain such loans. However, they generally have a ceiling (typically between ₹7.5 Lakhs to ₹10 Lakhs depending on the bank) and have a higher rate of interest.

2. Eligibility Criteria

While specific guidelines vary from one financial institution to another, the baseline eligibility criteria for an education loan in india include:

- Nationality: The applicant must be a citizen of India.

- Confirmed Admission: You must have secured admission to a recognized college, university, or institute through an entrance test or merit-based selection process.

- Age Limit – Usually, the student’s age should be between 16 and 35 years on the date of application.

- Co-Applicant Clause: The loan will require to be co-signed by a co-applicant (a parent, sibling or spouse) who has a steady income.

Also Read: 7 Game-Changing AI Tools to Scale Your reach Content Authentically

3. Mandatory Documents Checklist

To ensure your loan gets processed quickly without back-and-forth delays, keep the following documents ready before applying:

| Student’s Documents | Co-Applicant’s Documents |

| Academic Mark sheets (10th,12th,Graduation) | Past 6 months’ Bank Account Statements |

| Official Admission Letter from the College | Recent Salary Slips or Form 16 / ITR (Income Tax Return) |

| Detailed Fee Structure break-up from the Institute | KYC Documents (Aadhaar Card, PAN Card) |

| Identity & Address Proofs (Aadhaar, Passport, PAN) | Property/Asset documents (if applying for a secured loan) |

4. Step-by-Step Application Process

So many of the process when the bank is hard to handle. Adhere to this structural guideline to smoothly finish your journey of education loan in india:

Step 1: Research and Compare Options

Look for the best interest rates, processing charges, and hidden costs among the public and private lenders. You may also make use of the Government of India’s Vidya Lakshmi Portal for multiple bank loan schemes application and viewing.

Step 2: Submit the Loan Application Form

After you choose a bank, you can complete the application form online on their official website, or at your nearby bank branch. Fill in your personal details and financial requirements properly.

Step 3: Document Submission and Verification

For both you and your co-applicant, submit the paperwork. The academic credibility of your preferred college will be rigorously scrutinised by the bank, along with your credentials and the CIBIL score (credit history) of the co-applicant.

Step 4: Loan Sanctioning

If the bank’s credit department is satisfied with your profile, they will sanction your loan and send a formal Sanction Letter. It has important information such as the sanctioned loan amount, the variable interest rate and the tenure of repayment..

Step 5: Loan Disbursal

Once you sign the final contract, the bank will pay the tuition fee portion directly to the college or university’s official account in installments. As per the pre-agreed schedule, your living expenses, hostel fees or book allowance will be credited to your personal account.

Also Read: Summer Special Easy Recipe-Mango Mousse Recipe: Your Perfect Warm-Weather Treat

5. Loan Repayment and the Moratorium Period

One of the best things Indian Education loans have going for them is that you don’t need to start repaying right away.

What Is a Moratorium Period? Also referred to as a grace period, this is a fixed period that covers the Entire length of the course+ 6 months to 1 year (or until you get an employment, whichever is the earliest). You don’t have to pay any EMIs during this period. After this period has expired, your repayment term starts, which can be anywhere from 10 to 15 years.

Conclusion

Non availability of instant funds should not be a barrier to your dream of pursuing education. The financial bodies and the Government schemes are collaborating assisting the procedure of education loan in India to be easily available, transparent and free from trouble.

With the right research, a well-organized pack of documents and an application strategy, you can approach the funding system with confidence, knowing you’re well-equipped to finance that next step up in your career!